Quick Answer

A credit scoring system works by analyzing data from your credit report to produce a number between 300 and 850, where scores above 670 are generally considered good. The most widely used model is the FICO Score, which weighs payment history, amounts owed, credit history length, new credit, and credit mix. These scores remain the primary tool lenders use to evaluate borrower risk.

Lenders need a consistent way to measure risk across millions of applicants, and that is exactly what the FICO Score was built to provide. Created by Fair Isaac Corporation and used by the vast majority of top lenders in the United States, FICO scores are calculated from the information in consumers’ credit reports, including account balances and payment history, and are provided by the three major credit bureaus: Experian, Equifax, and TransUnion. Here we will discuss how the credit scoring system works.

Key Takeaways

- Credit scores range from 300 to 850, with scores above 670 considered good by most lenders, according to myFICO’s credit education guidelines.

- Payment history is the single largest factor in your FICO Score, accounting for 35% of the total calculation, as reported by the Consumer Financial Protection Bureau (CFPB).

- Amounts owed, also known as credit utilization, make up 30% of your FICO Score, making it the second most influential factor, per Experian.

- Approximately 90% of top lenders in the U.S. use FICO Scores when making credit decisions, according to Fair Isaac Corporation.

- VantageScore, a competing model developed jointly by Experian, Equifax, and TransUnion, uses the same 300–850 range but weights factors differently than the FICO model, as explained by NerdWallet.

1. How The Credit Scoring System Works

Scoring systems distill your entire borrowing history into a single number that represents creditworthiness. That number typically falls somewhere between 300 and 850, with higher values signaling lower risk to a lender. While several models exist, including FICO and VantageScore, most draw on the same core inputs: your credit report, public records such as bankruptcy filings, bureau updates on newly opened accounts, and payment records on existing obligations. The data gets fed into a scoring model and converted into a numerical value. The Federal Reserve has noted that these systems expand access to credit by giving lenders a standardized, objective measure of risk, as detailed in Federal Reserve research on credit scoring.

One important limitation worth naming: scoring models measure past behavior, not current ability to pay. Your income, job stability, and monthly cash flow do not factor into a FICO Score at all. That is why lenders typically evaluate the score alongside other information during underwriting.

2. Credit Score Formula

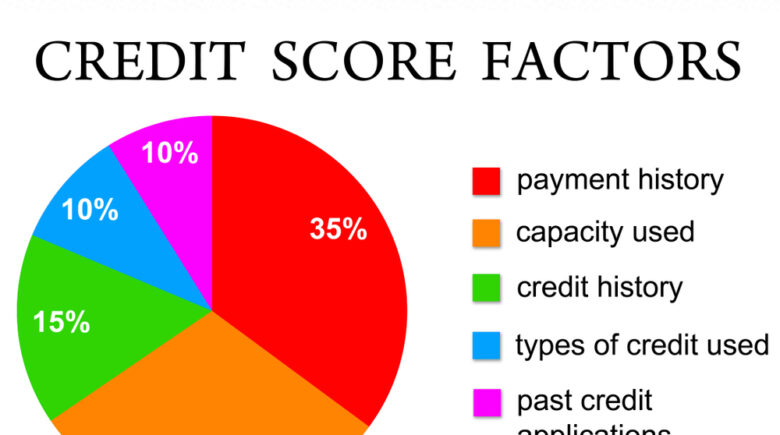

Five factors feed into the FICO calculation, according to the FICO Score breakdown published by myFICO: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%). The debt you carry relative to your available credit is among the most sensitive inputs. Longer credit histories generally help because they give the model more data points to evaluate. Importantly, the formula does not consider income or debt-to-income ratio (DTI), figures that lenders like Chase and SoFi often evaluate separately during the loan underwriting process. The formula tracks only how much you owe and how long those obligations have been active.

| FICO Score Factor | Weight | What It Measures | Example Impact |

|---|---|---|---|

| Payment History | 35% | On-time vs. late payments | One 30-day late payment can drop a score by 60–110 points |

| Amounts Owed (Credit Utilization) | 30% | Balances relative to credit limits | Keeping utilization below 30% is recommended |

| Length of Credit History | 15% | Age of oldest, newest, and average accounts | A 10-year-old account contributes more than a 1-year-old account |

| New Credit | 10% | Recent hard inquiries and new accounts | Multiple applications within 14–45 days may count as one inquiry |

| Credit Mix | 10% | Variety of credit types (cards, loans, mortgage) | Having both revolving and installment credit can help your score |

3. Components of Your Credit Score

The credit report compiled by Experian, Equifax, and TransUnion contains the raw material the scoring model works with: how much you owe, how many accounts you carry, how much creditors are owed, and how long you have had each account open. The CFPB outlines the full range of data that can appear on a consumer’s credit file in its credit reports and scores resource center. Among all those data points, the age of your credit history carries particular weight because it reflects how long lenders have been able to observe your behavior. Because the score is rooted in past actions, anything that happens to your accounts going forward will affect it. The Fair Credit Reporting Act (FCRA), enforced by the Federal Trade Commission (FTC), gives consumers the right to dispute inaccurate information on their credit reports, which can directly affect their scores.

4. Factors That Can Affect Credit Scores

Several variables shape where a score lands. These include the age of the individual’s oldest account and how long it has been open, the amount of debt owed on each account, the time between account openings, whether accounts have been paid in full or only partially, and whether any unpaid balances remain. According to Experian’s guide on factors that affect credit scores, even a single collection account can significantly lower a score, particularly for consumers who previously had strong credit histories.

The number of open credit cards and loans also matters. Carrying many balances suggests greater financial exposure, which scoring models treat as higher risk. The FDIC emphasizes that consumers should monitor their credit profiles regularly to identify potentially harmful changes early.

Closing an old credit card is a common misstep. Doing so can hurt a score by reducing total available credit and shortening the average account age. Keeping older accounts open, even with a zero balance, is often the better move from a scoring standpoint, as noted by the National Foundation for Credit Counseling (NFCC).

5. How Your Credit Score Is Affected By Your Credit History

The variety of credit you use also factors into the calculation. Holding both revolving accounts (credit cards) and installment accounts (auto loans, mortgages) gives the model a broader picture of how you handle debt. Someone applying for a mortgage for the first time will have a score that reflects only what the bureaus can observe so far. Someone with a long track record across multiple account types will generally score higher, all else being equal. Credit bureaus also factor in whether creditors have obtained a court judgment against you, which appears on your report as a “judgment” or “dishonor.” Lenders like SoFi and Chase frequently publish guidance on how different credit behaviors influence loan eligibility and annual percentage rate (APR) offers, because a higher FICO Score typically translates directly into lower borrowing costs for the consumer, as confirmed in NerdWallet’s analysis of credit scores and personal loan rates.

6. How to Improve Your Credit Score

Before taking any corrective steps, you need to know what is actually on your report. Get a free copy from each bureau through AnnualCreditReport.com, which is the only federally authorized source for free credit reports from Experian, Equifax, and TransUnion. Review every account, including negative items, and dispute anything that appears inaccurate.

From there, the highest-impact actions are paying bills on time, keeping old accounts open rather than closing them, and reducing card balances to bring utilization down. Avoid opening several new accounts at once, and if you need new credit, installment accounts tend to be less damaging to the score than multiple revolving lines. The CFPB also recommends setting up automatic payments to help ensure on-time payment history, which carries the greatest weight in the FICO formula, as detailed in the CFPB’s guide to building and maintaining a good credit score.

One honest caveat: improvement takes time. Paying down a large balance can lift a score within a billing cycle, but rebuilding a history damaged by late payments or collections typically requires years of consistent behavior. There is no shortcut for the length-of-history component, which accounts for 15% of the score.

Scoring is an ongoing process that spans industries far beyond traditional lending. Banks and credit card companies use scores to set interest rates, insurance companies use them to price policies, some employers review them during hiring, and landlords consult them before approving rental applications. Financial health and credit health are closely linked, and understanding what drives your score is the first step toward managing it deliberately.

Frequently Asked Questions

What is a credit score and why does it matter?

A credit score is a three-digit number between 300 and 850 that summarizes your creditworthiness based on your credit history. Lenders, landlords, insurers, and some employers use it when making decisions about you. A higher score typically means better loan terms, lower interest rates, and greater financial opportunities.

What is a good credit score?

According to myFICO, a score of 670 to 739 is considered “good,” 740 to 799 is “very good,” and 800 or above is “exceptional.” Scores below 580 are generally considered poor and may make it difficult to qualify for traditional credit products without a co-signer or secured collateral.

What is the difference between a FICO Score and a VantageScore?

The FICO Score is produced by Fair Isaac Corporation and is used by approximately 90% of top lenders in the U.S. VantageScore was developed collaboratively by Experian, Equifax, and TransUnion. Both use the same 300–850 range, but they weight factors differently. VantageScore gives more emphasis to credit utilization trends over time, while FICO places the most weight on payment history at 35%.

How often is a credit score updated?

Your score is recalculated each time a lender or bureau requests it, using the most current data in your report. Since lenders typically report updated account information to the bureaus once per month, meaningful changes to your score usually occur on a monthly basis.

What is the fastest way to improve a credit score?

Paying down high credit card balances is usually the quickest lever, since utilization accounts for 30% of your FICO Score. Disputing and removing inaccurate negative items can also produce rapid gains. Consistent on-time payments are the most impactful long-term strategy, though that improvement builds gradually rather than overnight.

How long does negative information stay on a credit report?

Most negative information, including late payments and collections, remains on your report for seven years from the date of the original delinquency. Bankruptcies can remain for up to ten years, depending on the type filed. After these periods, the information must be removed under the Fair Credit Reporting Act (FCRA).

Does checking your own credit score hurt it?

No. Checking your own score is a soft inquiry and has no effect on the number. Only hard inquiries, which occur when a lender pulls your credit as part of a formal application, can temporarily lower your score, typically by fewer than five points.

Can you have a credit score without a credit card?

Yes. Any type of credit account, including auto loans, student loans, or personal loans, can generate a score. Having no credit accounts at all means you may be “credit invisible,” a situation the CFPB estimates affects approximately 26 million Americans.

What credit score do you need to buy a house?

For a conventional mortgage, most lenders require a minimum FICO Score of 620. FHA loans backed by the Federal Housing Administration may be available with scores as low as 500 with a 10% down payment, or 580 with a 3.5% down payment. Higher scores generally unlock better mortgage rates and lower monthly payments.

How does credit utilization affect your score?

Utilization is the ratio of your outstanding card balances to your total credit limits, and it accounts for 30% of your FICO Score. Keeping that ratio below 30% is the standard recommendation, though consumers with the highest scores often stay below 10%. Paying down balances before the statement closing date can reduce your reported utilization even within the current billing cycle.

Do all lenders use the same credit score?

No. Different lenders may pull scores from different bureaus or use different FICO model versions. Mortgage lenders, for example, often use older FICO versions that may weigh factors slightly differently than the models used by credit card issuers. This means your score can vary depending on where a lender pulls it, even on the same day.

Sources

- Fair Isaac Corporation (FICO), FICO Score Overview

- myFICO, What’s in Your Credit Score

- Consumer Financial Protection Bureau (CFPB), What Is a Credit Score?

- Consumer Financial Protection Bureau (CFPB), Credit Reports and Scores Resource Center

- Experian, What Is a Good Credit Score?

- Experian, State of Credit Report

- AnnualCreditReport.com, Free Credit Reports from Experian, Equifax, and TransUnion

- Consumer Financial Protection Bureau (CFPB), How to Get and Keep a Good Credit Score

- Federal Reserve, Research Paper on Credit Scoring

- Federal Trade Commission (FTC), Fair Credit Reporting Act (FCRA)