Reviewed by the The Credit Scout Editorial Team

Our Take

For most freelancers expecting to owe $1,000 or more in federal tax, making quarterly estimated payments is not optional, it is a legal requirement, and skipping them costs money. The strongest system is to pay 100% of prior-year tax liability (110% if your prior-year AGI exceeded $150,000) each quarter, then reconcile in April. The case against this approach is a cash-flow one: safe harbor payments protect you from penalties but do not prevent a large April bill, which can blindside freelancers who assumed they had done everything right.

Freelancer estimated taxes trip up even experienced independent workers, not because the rules are complicated, but because the assumptions people bring from W-2 jobs are almost entirely wrong. According to the IRS Estimated Taxes guidance, self-employed individuals must pay as they earn, just like employees do through withholding. The difference is that nobody does it for you.

This article is for freelancers, sole proprietors, and independent contractors who are either new to quarterly payments or have been winging it for a few years and suspect they are doing it wrong. The recommendation here is specific and systems-based; where it breaks down, I will name it plainly.

Key Takeaways

- You owe quarterly estimated taxes once you expect to owe $1,000 or more in federal tax for the year, per IRS rules for self-employed filers, not based on gross revenue or total client payments.

- The self-employment tax rate is 15.3% on net earnings, per the IRS self-employment tax page, often larger than income tax itself, and the number most new freelancers forget to account for.

- The IRS quarterly calendar is deliberately uneven: Q2 covers only two months (April–May), while Q4 spans four, according to TurboTax’s quarterly tax guide. Treating all four quarters as equal windows is one of the most common and costly mistakes I see.

- The IRS underpayment penalty rate is 7% annualized for Q1 2026, per IRS Revenue Rulings compiled by ustax.tools. For a freelancer with a $22,000 tax bill who skipped all four quarters, actual penalty exposure is roughly $1,150, not the thousands that most articles imply.

- Freelancers with any W-2 income can increase their employer withholding late in the year and have it count as if paid evenly all year, a catch-up option that quarterly estimated payments cannot replicate. In my judgment it is one of the most underused tools available.

Why Freelancers Get the Basics Wrong Before They Even Start

The core problem is a psychological one: W-2 employees never see their tax money, so they cannot spend it. Freelancers receive gross payments in full and must mentally earmark the IRS’s share before spending the rest. Most don’t, at least not at first.

The actual trigger for quarterly payments is more specific than most people realize. According to the IRS Self-Employed Individuals Tax Center, you owe quarterly payments if you expect to owe $1,000 or more in federal tax after subtracting withholding and credits. That threshold is based on your tax liability, not on your gross revenue, your net profit, or how many clients paid you.

Thomas Mangold, CPA, ABV, CITP, CGMA, Partner at Aprio, has observed that many freelancers don’t even know estimated taxes exist until they face a penalty: “Those might not always be calculated into their withholding amount, and then they come up short and end up having to pay an estimated tax penalty and don’t even know what estimated taxes are.”

The compounding problem here: a freelancer who spends their tax money in year one often enters year two already in a hole. They owe April’s bill, then Q1 of the new year, and the gap widens. Getting behind on freelancer estimated taxes is easier than most people expect, and harder to recover from than most people want to admit.

The Trigger Is Not Revenue, It Is Tax Owed

A freelancer earning $40,000 in net profit may owe very little if they have significant deductions and credits. A freelancer earning $35,000 net with minimal deductions may cross the threshold easily. The IRS Publication 505 (2026 edition) includes a Form 1040-ES worksheet specifically for estimating this liability each quarter. The IRS recommends recalculating every quarter if your income projections change.

For freelancers who use payroll platforms like Gusto or accounting software like QuickBooks Self-Employed, some tools will estimate quarterly payments automatically, but they are only as accurate as the income and deduction data you feed them. Treat those estimates as a starting point, not a final answer.

What I see in practice: Readers who contact us after their first year of freelancing almost universally underestimated their bill because they calculated only income tax and forgot self-employment tax entirely. That omission alone can mean a shortfall of $6,000 to $10,000 on a mid-five-figure freelance income.

The Self-Employment Tax Shock Most Articles Bury

Self-employment tax is bigger than income tax for most freelancers in the $60,000 to $130,000 range, and ignoring it is the single most expensive quarterly tax mistake I can point to.

The SE tax rate is 15.3%: 12.4% for Social Security and 2.9% for Medicare, applied to 92.35% of your net self-employment earnings, not 100%. That 92.35% multiplier exists because employees only pay half the FICA rate; the other half comes from the employer. As a freelancer, you are both, so you pay both halves. But the IRS lets you calculate the base on 92.35% of net profit to approximate the employer-half deduction.

SE tax is separate from federal income tax, and it is also separate from any state income tax your state’s department of revenue may require. The Federal Reserve’s Survey of Consumer Finances has consistently shown that self-employed households carry wider income volatility than salaried households, which makes accurate SE tax estimation even more important for cash-flow stability.

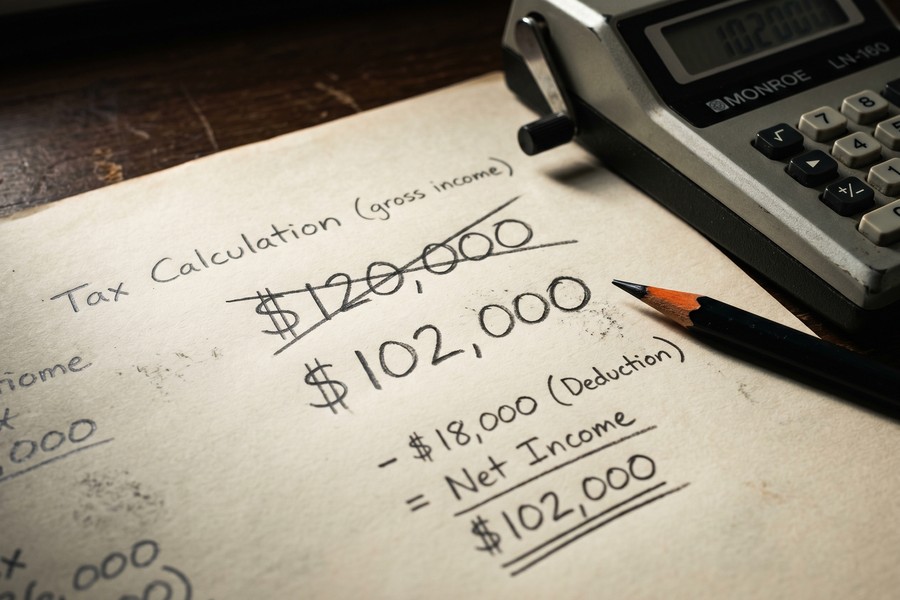

A Real Numbers Example

Here is the arithmetic on a concrete case. Take a freelancer with $120,000 gross income and $18,000 in business deductions, leaving $102,000 net profit. SE tax is calculated on 92.35% of that: $102,000 × 0.9235 = $94,197. SE tax: $94,197 × 15.3% = approximately $14,412.

Federal income tax on that same earner, after the above-the-line deduction for half the SE tax (roughly $7,206) and the 2026 standard deduction, would fall somewhere around $8,100 to $9,000 depending on filing status. SE tax exceeds income tax by nearly $6,000. Freelancers who calculate quarterly payments using only their income tax bracket are chronically underpaying from day one.

This gap matters beyond April 15. A large unexpected tax bill can push a freelancer to carry a balance on a Chase or Citi credit card at a high APR, or to drain an emergency fund that took months to build. The CFPB has noted in its annual financial well-being reports that irregular income earners are disproportionately likely to use revolving credit to cover tax obligations, a pattern that raises debt-to-income ratios and can suppress a FICO Score for months afterward.

What clients often miss: The 92.35% multiplier. Almost every freelancer I have helped recalculate their quarterly payment was applying SE tax to 100% of net profit, a small overestimate, but over four quarters it compounds into a meaningful miscalculation and leads to unnecessary anxiety about owing too much.

The Calendar Is Not What You Think

The IRS quarterly schedule is not four equal windows of three months each. Most freelancers assume it is, and that assumption costs them.

According to TurboTax’s quarterly tax guidance, the 2026 due dates are April 15, June 15, September 15, and January 15, 2027. That looks even until you map the income periods each covers:

| Quarter | Income Period | Months Covered | Due Date |

|---|---|---|---|

| Q1 | January – March | 3 months | April 15, 2026 |

| Q2 | April – May | 2 months | June 15, 2026 |

| Q3 | June – August | 3 months | September 15, 2026 |

| Q4 | September – December | 4 months | January 15, 2027 |

Q2 covers only two months. A freelancer who sets aside one-quarter of their projected annual tax for each period will underpay Q2 relative to the income earned in April and May. The penalty is calculated on that shortfall, per quarter.

The Q4 Opt-Out Rule Almost Nobody Mentions

Here is a detail missing from nearly every competing guide on estimated taxes: you can legally skip the January 15 Q4 payment entirely. The IRS Estimated Tax FAQ states that if you file your complete Form 1040 and pay the remaining balance in full by January 31, the January 15 quarterly payment is not required and no underpayment penalty applies to it. For freelancers who know their final numbers before month-end, filing early in January is a cash-flow option worth considering.

Safe Harbor Is a Penalty Shield, Not a Tax Strategy

Safe harbor is the most misunderstood concept in quarterly tax planning. It prevents underpayment penalties. It does not prevent a large April bill.

The rule: pay either 90% of your current-year tax liability or 100% of your prior-year tax liability across the four quarters, whichever is smaller, and the IRS will not assess an underpayment penalty regardless of what you owe in April. But if your income grew substantially, you could owe $15,000 or $20,000 on April 15 and still be penalty-free under safe harbor.

Riley Adams, CPA, Founder and CEO of Young and the Invested, puts the Form 1040-ES process clearly in his FinanceBuzz commentary on quarterly tax mistakes: “If it looks like you’ll owe more than $1,000 or more in taxes, however, you will want to use IRS Form 1040-ES to get a sense of how much you’ll make during the year and then determine and pay your estimated taxes based on these projections.” The implication is that safe harbor gives you legal cover, but accurately projecting current-year income and paying closer to 90% of actual liability is the better financial discipline.

The 110% Rule for Higher Earners

Freelancers whose prior-year adjusted gross income exceeded $150,000 must pay 110% of their prior-year tax liability, not 100%, to qualify for safe harbor. This rule is documented in IRS Publication 505, but it catches a significant number of freelancers mid-career who cross that threshold for the first time. If you earned $160,000 last year and based your quarterly payments on 100% of that prior-year bill, you are legally exposed on the 10% gap.

Understanding safe harbor is also essential if you are building financial stability as a self-employed worker. A large unexpected April liability can destabilize a credit profile and savings plan that took years to construct. Lenders using Experian or Equifax data to evaluate a mortgage or small-business loan application will see the downstream effects: elevated DTI from a tax payment plan, or a dip in FICO Score if a tax-related charge-off ends up on your credit file.

The Underpayment Penalty Is Smaller Than You Fear

The penalty math is almost never shown accurately in articles on this topic, and the omission makes freelancers either panic unnecessarily or avoid the topic entirely.

The underpayment penalty is not a flat fine. It is an interest charge, the federal short-term rate plus 3 percentage points, calculated separately per quarter on only the underpaid amount for that quarter. According to IRS Revenue Rulings tracked by ustax.tools, the annualized rate was 7% for Q1 2026 and dropped to 6% for Q2 2026. A separate failure-to-pay penalty of 0.5% of the balance per month applies only if you also fail to pay by April 15, as Riley Adams, CPA, notes in his FinanceBuzz analysis of quarterly tax mistakes.

Partial compliance genuinely reduces costs. Missing only Q3 and Q4 means no penalty accrues on Q1 and Q2. For a freelancer under $80,000 in net income who skipped all four quarters, actual penalty exposure is typically in the $200 to $400 range, not thousands. The anxiety around this number is almost always disproportionate to the dollar amount.

Irregular Income Freelancers Have a Better Option Nobody Uses

If your income is uneven across the year, a common reality for project-based freelancers, the standard quarterly payment approach penalizes you for slow periods that you had no control over.

The Annualized Income Installment Method, filed on Form 2210, Schedule AI, lets you calculate each quarterly payment based on actual year-to-date earnings rather than a flat projection of annual income. Per the IRS Estimated Tax FAQ, you can also mix methods, using the standard safe harbor method for quarters where it produces a lower required payment and switching to the annualized method for quarters where income was lower. The IRS accepts whichever method reduces your penalty, quarter by quarter.

This matters most for freelancers who earn heavily in Q3 and Q4 (common in media, consulting, and retail-adjacent work) and have little taxable income in Q1. If you are also working to build a spending plan around irregular income, the annualized method aligns your tax payments with your actual cash position rather than a hypothetical even-income projection. The catch is that Form 2210 adds complexity to your April return, but for freelancers with a significant slow season, the penalty savings usually justify it.

Thomas Mangold, CPA, ABV, CITP, CGMA, Partner at Aprio, has observed that many freelancers don’t even know estimated taxes exist until they face a penalty: “Those might not always be calculated into their withholding amount, and then they come up short and end up having to pay an estimated tax penalty and don’t even know what estimated taxes are.”

Where this gets tricky: Many readers skip Form 2210 because it looks intimidating. In practice, if you use tax software, the annualized worksheet is built in. You answer a few prompts about when income was earned, and the software does the quarterly math. The form itself does not need to be filed separately in most cases; it accompanies your 1040.

Where This Recommendation Falls Short

The quarterly safe harbor system works well for freelancers with relatively predictable income and a clear picture of last year’s tax return. It fails, sometimes badly, for several categories of readers.

The most honest drawback: safe harbor based on prior-year liability gives you penalty protection but does nothing to prevent a cash crunch in April. A freelancer who earned $80,000 last year, paid those prior-year taxes quarterly, and then earned $140,000 this year arrives at April 15 with a bill of $20,000 or more, penalty-free, but financially blindsided. The strategy optimizes for penalty avoidance, not for accurate prepayment. These are not the same thing.

The catch for first-year freelancers is more fundamental. You have no prior-year self-employment liability to base payments on, so the 100% safe harbor method is unavailable. You must estimate current-year income, an exercise that is genuinely hard when you are building a client base. Underpaying in year one is nearly universal, and the correct response is not to panic but to use the Form 1040-ES worksheet each quarter, update your projection as income materializes, and accept that the first year is a calibration exercise.

State estimated taxes are a second bill that this article addresses only briefly, but the risk is real. Forty-three states plus Washington D.C. impose income tax, and most have their own quarterly payment requirements with different thresholds, different due dates, and different penalty structures. Freelancers who relocated mid-year or work across state lines may owe in multiple states simultaneously, a scenario that the federal safe harbor system does not help you think through at all. Check your state’s department of revenue directly; do not assume the federal rules apply.

There is also a credit dimension worth naming. Entering an IRS installment agreement to pay an April balance raises your total debt load, which credit bureaus like Experian and TransUnion report to lenders. A higher debt-to-income ratio can affect approval odds on a SoFi personal loan, a small-business line of credit from Chase, or an FDIC-insured bank product you apply for later in the year. The CFPB’s guidance on installment agreements does not flag this risk explicitly, but any new monthly obligation increases your DTI, and lenders using FICO Score models will price that accordingly.

Finally: as of September 30, 2025, the IRS no longer accepts physical checks for estimated tax payments. If you have been mailing checks, that method is now closed. Use IRS Direct Pay, EFTPS, or a debit/credit card through an IRS-authorized processor. Several evergreen guides on freelancer estimated taxes have not updated their payment sections to reflect this change, worth knowing before you rely on outdated instructions.

For freelancers who also want to reduce what they owe in April, not just protect against penalties, the more useful strategy is aggressive and accurate deduction-tracking. Our guide to self-employed tax deductions you might be missing covers the categories that reduce your net profit, and therefore your SE tax base, before you ever calculate a quarterly payment.

How We Sourced This

This article draws primarily from IRS official publications, specifically the IRS Estimated Taxes page, IRS Publication 505 (2026 edition), the IRS Self-Employed Individuals Tax Center, and the IRS Estimated Tax FAQ, supplemented by verified expert commentary from Riley Adams, CPA (via FinanceBuzz) and Thomas Mangold, CPA (via NerdWallet). Penalty rate data for Q1 and Q2 2026 comes from IRS Revenue Rulings 2025-7, 2025-11, 2025-18, and 2025-23 as compiled by ustax.tools. The quarterly due-date calendar was verified against TurboTax’s 2026 quarterly tax guide. All data was verified; IRS penalty rates and safe harbor thresholds are subject to annual revision and should be confirmed directly with IRS.gov before filing. The payment-method change (checks no longer accepted as of September 30, 2025) is sourced from IRS communications and reflected in current IRS online guidance.

Frequently Asked Questions

How do I know if I owe freelancer estimated taxes?

You owe quarterly estimated taxes if you expect to owe $1,000 or more in federal tax after subtracting withholding and credits. Use the Form 1040-ES worksheet from the IRS to estimate your liability each quarter, and recalculate if your income changes significantly mid-year.

What happens if I miss a quarterly estimated tax payment?

Missing a payment triggers an underpayment penalty calculated at the federal short-term rate plus 3 percentage points, 7% annualized for Q1 2026, applied only to the underpaid amount for that specific quarter. For most freelancers earning under $80,000, the actual dollar penalty for missing all four quarters is typically $200 to $400, not thousands. Paying late is still better than not paying at all.

Can I skip the January 15 fourth-quarter payment?

Yes. If you file your complete Form 1040 and pay your remaining tax balance in full by January 31, the IRS does not require the January 15 estimated payment and assesses no penalty for skipping it. This is a documented IRS rule that most guides omit entirely.

What is the safe harbor rule for estimated taxes?

Safe harbor means paying either 90% of your current-year tax liability or 100% of your prior-year tax liability across four quarters, whichever is smaller, and facing no underpayment penalty regardless of what you owe in April. If your prior-year adjusted gross income exceeded $150,000, the threshold rises to 110% of prior-year liability. Safe harbor prevents penalties but does not prevent a large April balance.

Should I use the annualized income installment method if my income is uneven?

For freelancers with a significant slow season or unpredictable income timing, the Annualized Income Installment Method (Form 2210, Schedule AI) calculates each quarterly payment based on actual year-to-date earnings rather than a projected annual figure, and can legally reduce or eliminate penalties after a low-income quarter. Most tax software handles this automatically if you enter when income was earned. The tradeoff is that it adds a layer of complexity to your April return, but the penalty savings usually justify the extra step for irregular earners.

Sources

- Internal Revenue Service, Estimated Taxes (Self-Employed)

- Internal Revenue Service, Publication 505 (2026): Tax Withholding and Estimated Tax

- Internal Revenue Service, Self-Employed Individuals Tax Center

- Internal Revenue Service, Estimated Tax FAQs

- Internal Revenue Service, Self-Employment Tax (Social Security and Medicare Taxes)

- Intuit TurboTax, A Guide to Paying Quarterly Taxes

- ustax.tools, IRS Estimated Tax Penalty Calculator (Revenue Rulings 2025-7 through 2025-23)

- FinanceBuzz, Quarterly Tax Mistakes to Avoid (featuring Riley Adams, CPA)

- NerdWallet, Estimated Quarterly Taxes: What They Are and How to Pay (featuring Thomas Mangold, CPA)

- Internal Revenue Service, IRS Direct Pay