Fact-checked by the The Credit Scout editorial team

Quick Answer

The biggest money management mistakes new graduates make include spending based on gross salary instead of net take-home pay, ignoring student loan grace periods, skipping employer 401(k) matches, and failing to build any emergency fund. Most new grads earn an average starting salary of $56,153, yet expect roughly $80,000, creating a structural budget gap that drives nearly every other financial misstep in year one.

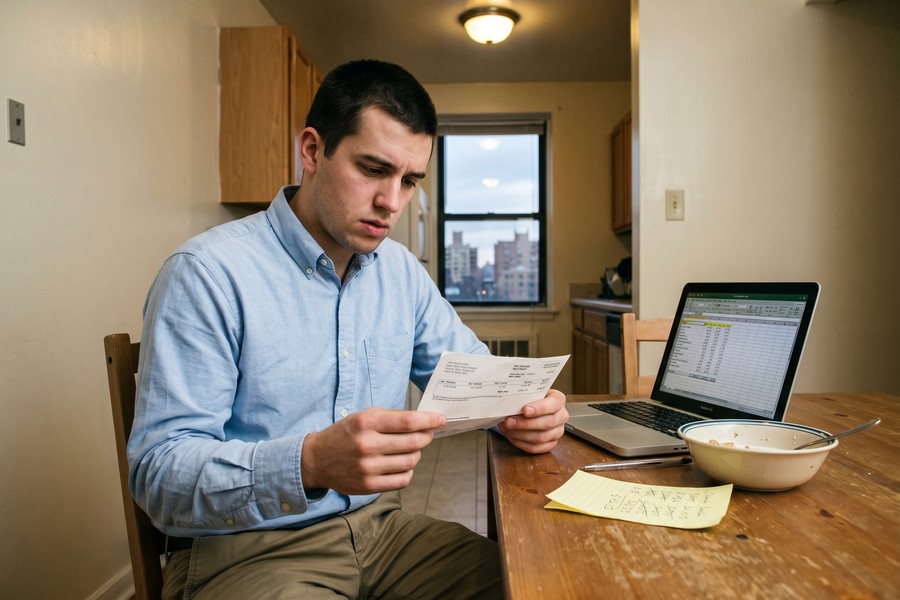

The money management mistakes new graduates make are largely predictable, and they tend to cluster in the first twelve months when income feels real but financial habits do not yet exist. According to LendingTree’s 2025 student loan data, the average Class of 2024 bachelor’s degree recipient left school carrying $29,560 in federal and private student loan debt, and that balance begins accruing repayment obligations before most new hires have figured out their first paycheck. The structural collision of rent, taxes, loan payments, and health insurance premiums arriving simultaneously is not a failure of motivation. It is a predictable consequence of zero formal financial education.

This guide names the six mistakes that cause the most damage in year one, explains why each one happens, and gives you the specific numbers and decisions that change the outcome. If you are about to graduate, recently hired, or watching someone you care about start their first real job, the next few months matter more than most people realize.

Key Takeaways

- The average new graduate starting salary is $56,153, nearly $24,000 below what most college seniors expect to earn, making lifestyle plans built on offer-letter numbers structurally unworkable from day one (per CNBC/Clever, 2026).

- 20% of student loan borrowers were behind on payments or in collections in 2024, up from 16% the year before, according to the Federal Reserve’s 2025 Household Well-Being Report.

- 55% of Gen Z adults lack enough emergency savings to cover three months of expenses, per Bank of America’s 2025 Better Money Habits study, leaving new graduates especially exposed to the first unexpected expense.

- 61% of young people are not saving for retirement, according to a 2024 CNBC and Generation Lab survey cited by Inside Higher Ed, meaning most new hires are leaving employer 401(k) match money uncollected.

- 59% of Americans cannot cover an unexpected $1,000 emergency from savings, per Bankrate’s 2025 Emergency Savings Survey via CBS News, a figure that captures exactly where most new graduates start their financial lives.

In This Guide

- Why the First 12 Months Are a Financial Minefield

- Are You Budgeting Off Your Offer Letter Instead of Your Paycheck?

- How Lifestyle Creep Starts Before the First Paycheck Clears

- What Should You Actually Do During the Student Loan Grace Period?

- Why Employer Benefits Are a High-Stakes Financial Decision

- Skipping the Emergency Fund Because Debt Feels More Urgent

- The Long-Term Cost of Not Negotiating Your First Salary

- Frequently Asked Questions

Why the First 12 Months Are a Financial Minefield

The transition from student to employed adult is not a gradual slope. It is a hard discontinuity. Within weeks of graduation, a new hire may face their first lease, their first payroll tax withholding, their first health insurance enrollment decision, and the ticking clock of a student loan grace period, all at the same time. Most universities provide no structured preparation for this moment.

The Literacy Gap Is Structural, Not Personal

The mistakes described throughout this article are not primarily about discipline or effort. They are the predictable output of a system that graduates students carrying tens of thousands in debt while providing almost no instruction on managing it. Understanding that framing matters because it shifts the response from shame to strategy.

The 2025 to 2026 job market adds another layer of pressure. The recent-graduate unemployment rate reached approximately 5.3% in mid-2025 according to the New York Federal Reserve, compared to roughly 4% for the broader labor force. For a meaningful share of graduates, the financial squeeze begins before the first paycheck, not after. A realistic financial plan for year one must account for the possibility of a gap between graduation and first employment, yet almost no generic budgeting advice acknowledges this.

About half of parents are now covering essential monthly expenses, including groceries, rent, and utilities, for their recent graduate children, according to a 2025 Savings.com survey. This informal subsidy often masks poor financial habits until the support ends, which is frequently the real first financial test.

Are You Budgeting Off Your Offer Letter Instead of Your Paycheck?

Spending plans built on a gross salary number fail immediately. Federal income tax, FICA contributions for Social Security and Medicare, state income tax, health insurance premiums, and any 401(k) contribution can collectively reduce a $68,000 offer to under $50,000 in actual take-home pay. That is not a rounding error. It is a structural gap that determines whether a lease is affordable before the lease is signed.

The Expectation Reality Gap

Today’s college seniors expect to earn approximately $80,000 in their first year after graduation. The actual average starting salary documented by Clever in early 2026 is $56,153. That nearly $24,000 shortfall is not a minor calibration problem. It means that the apartment, the car payment, and the discretionary spending plan a new graduate built in their head during senior year are already broken before orientation week ends.

The fix is straightforward: run a paycheck audit before signing any recurring financial commitment. Use your offer letter salary, subtract estimated federal and state taxes, subtract FICA (7.65% of gross pay), subtract any health insurance premium your employer quotes, and look at what remains. That number, not the offer letter, is your budget. For guidance on structuring a spending plan around irregular or newly predictable income, the framework in our guide on building a spending plan without a steady paycheck translates well to first-year employees navigating their first real budget.

How Lifestyle Creep Starts Before the First Paycheck Clears

Lifestyle creep is the quiet expansion of spending to match a new income level, and it typically starts the moment a new hire signs an offer letter. The psychological shift from “broke student” to “employed adult” feels like permission to upgrade everything at once: the apartment, the wardrobe, the furniture, the subscriptions.

The Subscription Stack Problem

One of the least-discussed drivers of this creep is the subscription economy. New graduates entering independent adult life for the first time tend to activate streaming services, gym memberships, meal kit deliveries, cloud storage plans, and productivity software in rapid succession. These individual charges feel small. The total rarely does.

The average U.S. household now spends $273 per month on subscriptions, a figure that has climbed dramatically over the past several years. New graduates are particularly vulnerable because they are often entering these services for the first time across multiple categories simultaneously, with no baseline to measure against. A useful counter-move is to run a subscription audit in month one: list every recurring charge, assign it a dollar figure, and decide which ones survive a strict cost-benefit review. The comparison framework in our guide on buying versus subscribing offers a practical decision structure for exactly this kind of review.

The only reliably effective defense against lifestyle creep is automation. Setting up an automatic transfer to a savings account on payday, before discretionary spending begins, removes the choice entirely. Willpower is not a reliable financial strategy.

Set up your savings transfer on the same day as your direct deposit, not at the end of the month. Money that never appears in your checking account rarely gets spent. Even a $100 automatic transfer builds the habit and the account simultaneously.

What Should You Actually Do During the Student Loan Grace Period?

Most federal student loans come with a six-month grace period after graduation before repayment begins. The correct use of that window is active financial planning, not passive waiting. The common mistake is treating the grace period as free time when it is actually the best planning window a new graduate will ever have before the stakes get real.

What to Calculate Before the First Bill Arrives

The Consumer Financial Protection Bureau advises new graduates to understand every federal and private repayment option available to them before their grace period ends, including income-driven repayment plans, and warns explicitly that missing even a single payment can trigger late fees, additional interest, and lasting credit damage.

“It wasn’t until about six months after I graduated, which was when my grace period ended for me…that I started thinking about my student loan.”

Hamilton’s experience is the norm, not the exception. The financial literacy gap around student loans is measurable: CFPB guidance consistently shows that graduates who engage with repayment planning tools before the grace period ends are substantially better positioned to avoid default. During those six months, a graduate should log into their federal loan servicer account, confirm every loan balance and interest rate, model the monthly payment under both the standard ten-year plan and any income-driven options, and compare the long-run interest cost of each.

Income-driven repayment deserves a direct caveat here. It can make monthly payments manageable when income is low, but it does not reduce total debt. It often increases it. The honest trade-off is lower short-run payments in exchange for higher long-run interest costs, sometimes significantly higher. That trade-off is worth making in specific circumstances, but it should be made with full information, not by default. If you are weighing debt paydown against building a cash cushion, the detailed breakdown in our post on whether to pay off debt first or build an emergency fund is directly applicable here.

| Repayment Plan | Monthly Payment (on $29,560 at 6.5%) | Total Interest Paid |

|---|---|---|

| Standard (10-Year) | $335/month | $10,653 |

| Extended (25-Year) | $198/month | $29,978 |

| Income-Driven (SAVE) | Varies by income; floor near $0 if income is low | Highest over time; balance may grow |

Why Employer Benefits Are a High-Stakes Financial Decision

Benefits enrollment paperwork feels like administrative noise during onboarding week. It is not. The decisions made in that window, often under time pressure within the first 30 days of employment, can shift take-home pay by hundreds of dollars per month and affect retirement account balances by tens of thousands of dollars over a career.

The 401(k) Match Is Not Optional Money

An employer 401(k) match is the single highest guaranteed return available to most new employees. If an employer matches 50% of contributions up to 6% of salary, contributing that 6% delivers an immediate 50% return on those dollars before any market growth. The American Bankers Association explicitly identifies failing to take advantage of the employer 401(k) match as one of the primary financial traps for new graduates.

The compounding math is unambiguous. One thousand dollars invested at age 22 at a 7.2% average annual growth rate grows to approximately $32,000 by age 70. That same $1,000 applied to a 5% student loan saves roughly $50 in interest over the life of the loan. The asymmetry is stark, which is why capturing the full employer match should take priority over accelerated debt paydown in nearly every scenario where the debt interest rate is below 7%.

Delaying 401(k) enrollment by even one year in your twenties is a quantifiable cost, not a neutral decision. For new graduates who want a structured approach to building retirement savings from scratch, our breakdown of Roth IRA versus Traditional IRA options covers the tax trade-offs that apply starting in year one.

Health Insurance Tier Selection Matters More Than Most Realize

Choosing a higher-premium health insurance tier when a lower-premium high-deductible plan paired with a Health Savings Account (HSA) would be more appropriate is a surprisingly common mistake. A healthy 22-year-old paying $200 more per month in premiums for a low-deductible plan than they need is spending $2,400 per year unnecessarily. The math depends on actual healthcare usage, but the decision should be deliberate, not default.

61% of young people are not saving for retirement at all, according to a 2024 CNBC and Generation Lab survey. For new graduates, that statistic represents employer match money left uncollected and compounding time that cannot be recovered.

Skipping the Emergency Fund Because Debt Feels More Urgent

The instinct to attack student loan debt as fast as possible is understandable, but entering the workforce with zero emergency savings while carrying debt is a riskier position than carrying debt while maintaining a small cash buffer. A single unexpected expense, a car repair, a medical bill, an emergency flight home, forces a graduate with no savings onto a high-interest credit card, which creates a new, costlier debt problem on top of the existing one.

A Realistic Year-One Target

The standard advice to save three to six months of expenses before doing anything else is correct in principle and often impossible in practice for a new graduate earning $56,000 in a high-cost city. A more realistic sequencing: build a starter emergency fund of $1,000 to $2,000 first, then capture the full employer 401(k) match, then address debt aggressively. The starter fund stops the bleeding without requiring a year of austere saving before any other financial goal is addressed.

The data on where most new graduates actually stand is sobering. According to Bank of America’s 2025 Better Money Habits study, 55% of Gen Z adults lack enough savings to cover three months of expenses. And per Bankrate’s 2025 Emergency Savings Survey, 59% of Americans cannot cover an even smaller $1,000 emergency from existing savings. New graduates are not outliers on this measure. They are the median.

“This often leads students to rely on credit cards or loans, compounding their financial troubles.”

Kovar’s observation applies directly to new graduates who skip emergency savings under the assumption that debt paydown is the more responsible priority. Without a cash buffer, any financial disruption routes directly to revolving credit, and credit card interest rates currently make that a very expensive emergency response. The credit consequences of leaning too heavily on credit cards in year one are also lasting. Our article on credit building mistakes that are actually making your score worse covers several that are specific to this pattern.

The Long-Term Cost of Not Negotiating Your First Salary

Accepting the first offer without negotiating is one of the most expensive single decisions a new graduate makes, and its cost compounds for years. Future raises, competing offers, and employer counteroffers are frequently anchored to current base salary. A $3,000 first-year negotiation win, modest by any standard, can translate into tens of thousands of dollars of additional lifetime earnings when that base propagates through a career.

What Negotiation Actually Looks Like in Practice

Most new graduates skip negotiation because they fear losing the offer. That fear is almost always disproportionate. Employers expect negotiation, and a professional, reasoned request for a salary adjustment rarely threatens an offer that has already been extended. The framing that works best is factual rather than personal: “Based on my research into market rates for this role in this area, I was hoping we could discuss a starting salary closer to X.” That is not entitlement. It is market awareness.

When base salary is genuinely fixed, the negotiation moves to benefits. Signing bonuses, remote work stipends, additional vacation days, and professional development budgets all carry real dollar value and are often more flexible than base pay. Benefits negotiation is an underused lever that most generic advice on money management mistakes new graduates ignore entirely.

The honest caveat: negotiation carries a small but real risk of creating friction in a new employment relationship, particularly in more hierarchical organizations. Knowing the culture before negotiating matters. The strategy that works at a startup may land differently at a large institution. That said, the asymmetric risk calculation still favors negotiating: the worst realistic outcome is usually a polite “no,” while the best outcome has a compounding return across an entire career.

Understanding how your compensation connects to your tax situation also matters in year one. Our guide to 2026 tax brackets and how to identify yours is a practical starting point for understanding how a salary bump affects your effective tax rate and net take-home pay.

According to the Federal Reserve’s 2025 Household Economic Well-Being report, 20% of student loan borrowers were behind on payments or in collections in 2024, up from 16% in 2023. Late payments on student loans report to the major credit bureaus, Equifax, Experian, and TransUnion, and can stay on a credit report for seven years.

Building strong credit from the foundation up is a related priority in year one. Graduates who want to understand the full arc of that process will find the step-by-step story in our post on how a recent college graduate built a 700+ credit score in under two years both instructive and realistic about the timeline involved.

Frequently Asked Questions

What is the most common money management mistake new graduates make?

The most common mistake is building a spending plan around gross salary rather than actual take-home pay after taxes and deductions. This single error causes new graduates to overcommit on rent, car payments, and lifestyle expenses before they have seen a real paycheck, creating a budget deficit that is difficult to unwind.

How much should a new graduate save in their first year?

A realistic first-year savings target starts with a $1,000 to $2,000 emergency fund before any other savings goal. After capturing the full employer 401(k) match, a new graduate earning around $56,000 should aim to save at least 10% of net income, though the exact figure depends on cost of living and debt obligations. The goal in year one is establishing the habit and the systems, not hitting an aggressive savings rate immediately.

Should I pay off student loans or build an emergency fund first?

Build the starter emergency fund first, then capture the employer 401(k) match, then accelerate student loan paydown. Zero emergency savings while carrying debt is a riskier position than it appears because any unexpected expense will route to high-interest credit cards, creating a new and more expensive debt problem. A $1,000 to $2,000 cash buffer prevents that outcome.

What should I do during my student loan grace period?

Use the six-month federal grace period as a planning window, not a spending window. Log into your loan servicer account, confirm every balance and interest rate, model monthly payments under the standard ten-year plan and any income-driven alternatives, and select your repayment plan before the first bill arrives. The Consumer Financial Protection Bureau provides free tools to compare every option available to you.

How does skipping the 401(k) match affect long-term finances?

Skipping the employer 401(k) match is effectively declining part of your compensation. One thousand dollars invested at age 22 at a 7.2% growth rate grows to approximately $32,000 by age 70. Delaying enrollment by even one year in your twenties is a permanent loss of compounding time, not a recoverable one. Capturing the full match is the highest-priority financial action available to most new employees.

Is salary negotiation worth the risk as a new graduate?

Yes, in almost every case. The realistic downside of a professional salary negotiation request is a polite decline. The upside, a $3,000 to $5,000 first-year increase, compounds through future raises and job offers anchored to your current salary. The asymmetry strongly favors asking, especially when the request is framed around market data rather than personal need.

What is lifestyle creep and how do new graduates avoid it?

Lifestyle creep is the gradual expansion of spending to match new income, and it typically starts the moment a graduate receives an offer letter. The most effective prevention is automating savings transfers on payday before discretionary spending occurs, and auditing all subscription services within the first 30 days of employment. Spending that is never available to spend never gets spent.

Sources

- LendingTree, Student Loan Debt Statistics 2025

- Federal Reserve, Report on the Economic Well-Being of U.S. Households in 2024: Higher Education and Student Loans

- CBS News, Bankrate 2025 Emergency Savings Survey: Most Americans Cannot Cover a $1,000 Expense

- Bank of America Newsroom, Better Money Habits 2025 Study: Gen Z and Emergency Savings

- Inside Higher Ed, Helping College Students Save for Retirement (CNBC/Generation Lab 2024 Survey)

- Consumer Financial Protection Bureau, Federal and Private Student Loan Repayment Options

- Consumer Financial Protection Bureau, A Resolution to Conquer Your Student Debt

- American Bankers Association, Financial Traps for College Graduates

- GoBankingRates, Money Mistakes Commonly Made by New Grads and What to Do Instead (Taylor Kovar, CFP)

- CollegeData, Common Money Mistakes College Students Make (Kimberly Hamilton, CFEI)